Empowering Entrepreneurs through UPI and Digital Wallets: Assessing Their Role in Financial Inclusion and Enterprise Growth in India

Article Sidebar

Main Article Content

Abstract

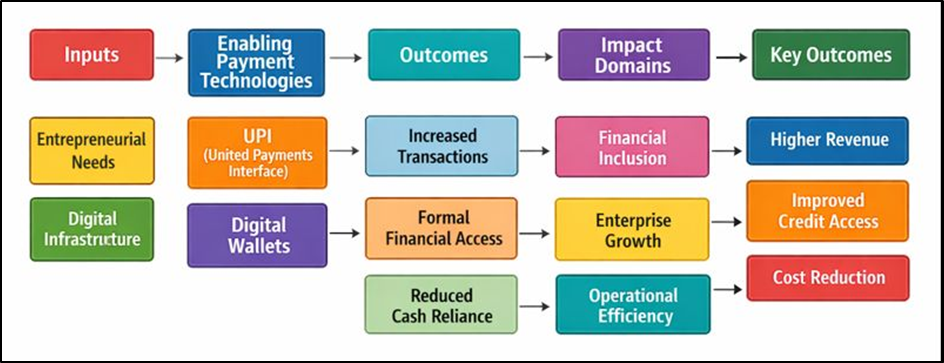

The fast growth of digital payment ecosystems in India, which is driven by the Unified Payments Interface (UPI) and digital wallets, has radically reshaped the entrepreneurial finance and operations of the business. This paper discusses the importance of UPI and digital wallets in enhancing financial inclusion and enabling the growth of enterprises among entrepreneurs; specifically the micro, small, and medium enterprises (MSMEs). The study is based on a mixed-method empirical approach, where survey-based primary data of entrepreneurs in urban and rural areas and secondary data of national payment statistics and fintech reports are combined. These are the adoption drivers, intensity of use, efficiency of transactions, and transparency, which are systematically examined to gain insight on behavioural and structural determinants that affect the uptake of the digital payment. The results suggest that UPI and digital wallets significantly decrease the transaction cost, increase the speed of payments, and financial visibility, in turn, decreasing the use of cash and unstructured financial activities. Enhanced access to institutional financial services, such as savings, credit, and insurance services, is also brought out as a major route through which the digital payments enhance financial inclusion. Record of transactions made by digital platforms also assist in assessing creditworthiness, as well as access to formal credit becomes easier among the businesspeople. Regarding the enterprise performance, there are increased volumes of transactions, better revenue stability, efficiency of operations, and increased market penetration associated with digital payment adoption. As can be seen through comparative analysis, UPI is more scalable and interoperable whereas digital wallets provide value added services that can be useful in customer engagement.